Balancing Act: Navigating Vodafone Idea's Debt Dilemma and the GOI's Equity Gamble

Balancing Act: Navigating Vodafone Idea's Debt Dilemma and the GOI's Equity Gamble

Vodafone Idea's survival hinges on strategic debt management and operational efficiency to ensure its competitiveness and the overall health of India's telecom sector

In a notable move, the Government of India (GOI) converted the interest payment obligations of Vodafone Idea (VI) during the moratorium period into preferential equity. This strategic decision resulted in the GOI acquiring a 32.09% stake in the company, equating to access to 16.13 billion shares, as detailed on page 18 of the EGM minutes dated January 31, 2023. The total interest amount considered for this conversion was approximately Rs 16,000 crore. According to a Press Information Bureau release dated September 25, 2021, this initiative aimed to alleviate financial stress in the telecom sector and preserve its competitiveness. This article seeks to analyze whether the GOI should sell its shares in VI post-moratorium and project the potential ownership trajectory from 2025 onwards, following the moratorium's expiry on September 25, 2025.

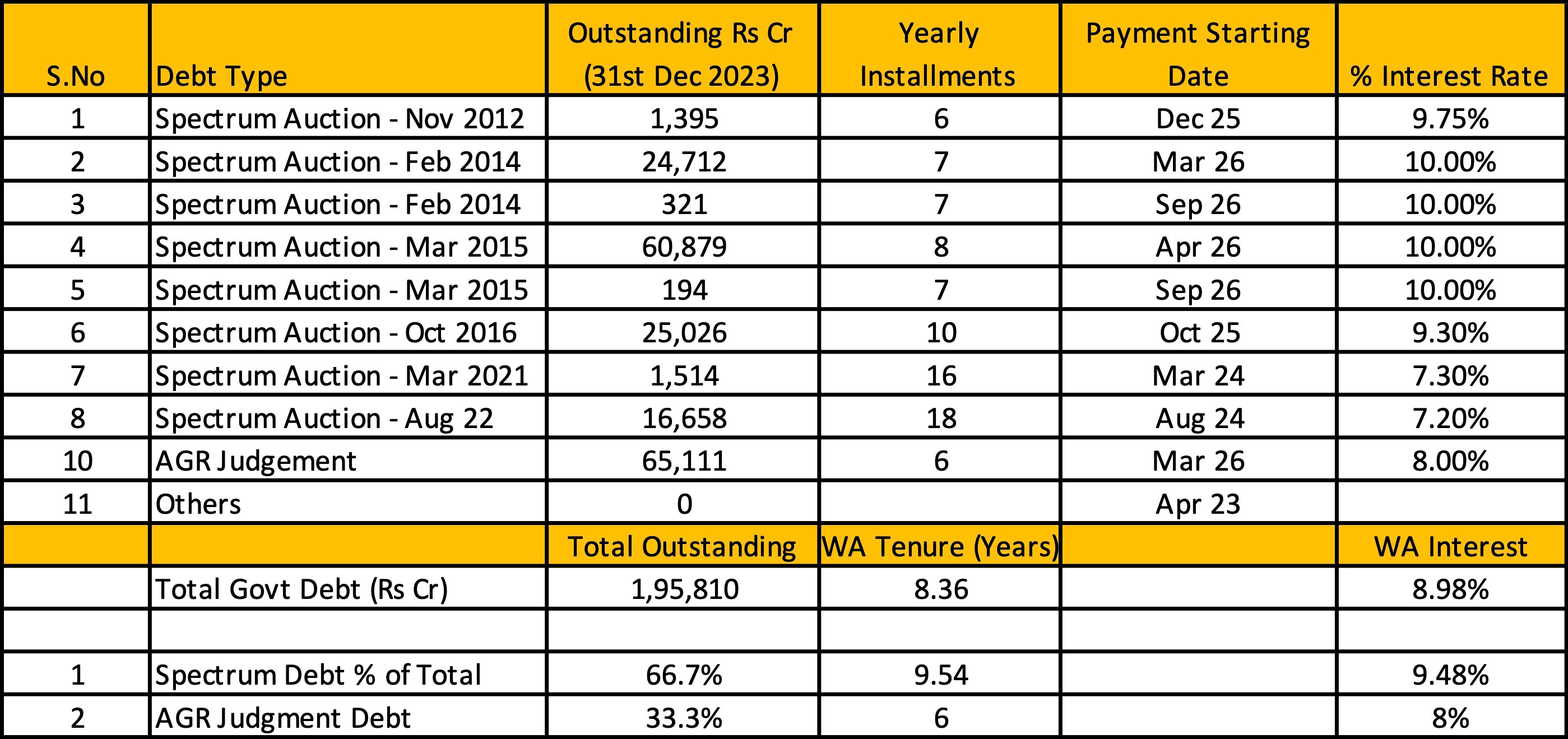

VI’s Yearly Payment Obligation to the GOI from FY25

The data below, extracted from Vodafone Idea's (VI) latest annual report, outlines VI's yearly payment obligations to the Government of India starting from the financial year 2025. It's important to note that these figures do not account for the cash outflows from the recent spectrum auction in 2024, which are expected to be marginal.

At the conclusion of the moratorium period, VI's annual payment obligation to the Government will amount to approximately Rs 36,790 crore. For details on the formula used to calculate these yearly installments, please refer to my previous note, linked here. Of this total, dues from the Adjusted Gross Revenue (AGR) judgment constitute Rs 14,084 crore, representing 38% of the total obligation.

GOI’s Percentage Holding of the Company at Various Share Prices

Assuming the Government of India (GOI) maintains its current holdings and opts to convert a rounded debt of Rs 40,000 crore due in FY26, it's evident that Vodafone Idea (VI) — with revenues projected in the same range — will be unable to make this repayment. According to the latest shareholding data post-FPO, the GOI's holding would decrease from 32.09% to 24.27%, representing ownership of 16.13 billion shares out of a total 66.46 billion (calculated as 16.13 / 0.2427).

Scenario Analysis at Different Share Prices:

Case 1: Shares Acquired at Rs 15 Each

If GOI acquires a new tranche of 26.66 billion shares (calculated as 4000 crore / Rs 15), the total share count would increase to 93.12 billion. Consequently, GOI’s stake would rise to 45.95%, based on holding 42.79 billion shares (16.13 billion existing + 26.66 billion new).

Case 2: Shares Acquired at Rs 20 Each

With shares priced at Rs 20 each, GOI would need to be issued 20 billion new shares. This would adjust the total shares to 86.46 billion and increase GOI’s stake to 41.17%, holding 36.13 billion shares.

Case 3: Shares Acquired at Rs 25 Each

At a share price of Rs 25, GOI would acquire 16 billion new shares, raising the total to 82.46 billion shares. This would result in GOI holding 38.96% of the company, with 32.13 billion shares in total.

Possible GOI Strategy Going Forward

Given that Vodafone Idea (VI) faces a continuous outflow of Rs 40,000 crore annually for 6 to 7 years following the end of the moratorium period, and considering the need for further debt to acquire new spectrum and deploy new technology to remain competitive, it is crucial for the GOI to manage its holdings in VI strategically. The aim should be to prevent an excessive increase in its stake, which could lead to the dilution of other important stakeholders and create structural issues within the company.

A practical approach for the GOI would be to progressively reduce its holdings each year as the company's stock price increases. This strategy allows the GOI to decrease its percentage ownership in a controlled manner, reducing exposure while maximizing potential gains from rising stock values. For instance, if the GOI were to sell its 16.13 billion shares now, by FY26, its holdings would decrease to 28.62% under Case 1 conditions, 23.13% under Case 2, and only 19% under Case 3. Such a strategy would position the GOI more favorably ahead of the next major payment due in FY27, ensuring the situation remains manageable.

Conclusion

Vodafone Idea's (VI) financial health is precarious, necessitating astute management and strategic oversight from the Department of Telecommunications (DoT). To avoid a financial crisis driven by hefty debt payments and the Government of India's (GOI) significant equity exposure, it is imperative that VI rapidly transitions to cash flow positivity and curtails its losses. This improvement in financial health is crucial for enabling the GOI to implement a gradual share divestiture strategy, ideally timed with appreciating stock values, as new debts mature for payment.

A critical element of this strategy hinges on VI's ability to boost revenue significantly, potentially obviating the need for full debt-to-equity conversions if cash generation becomes sufficient. Furthermore, alleviating the burden of Adjusted Gross Revenue (AGR) obligations, which constitute nearly 40% of VI's total governmental debt, could provide significant relief and stability.

Looking forward, VI's path is fraught with challenges, but with continuous support from the GOI—ensuring the company stands independently and meets its financial obligations without resorting to further equity conversions—the future could be more promising. The survival and competitive viability of VI are not only vital for its stakeholders but also for maintaining a robust, consumer-friendly telecom market in India. As such, all stakeholders must remain hopeful and committed to navigating these complexities for the greater good of the industry and its consumers.

Well articulated. Scenarios of subs retention and revenue growth are key to analyse