Analyzing Spectrum Pricing for Indian Satellite Services

Analyzing Spectrum Pricing for Indian Satellite Services

The total outflows within the Satellite Industry due to spectrum allocation MUST NOT surpass 1% in aggregate

Debate is on in India, whether the spectrum of satellite service should be auctioned or must be given administratively. In both situations, the regulators will face the task of estimating the pricing of the satellite spectrum. The strategy for estimating the price can be many. But to check whether we are in the ballpark range one can use the outflow of spectrum prices (applicable to the Indian telecom Industry) as a reference. This note calculates the Total Industry Outflow for spectrum auctions since 2010 and compares the same with the Industry’s Gross Revenue, and using this information makes an attempt to estimate the price of the satellite spectrum.

Assumptions

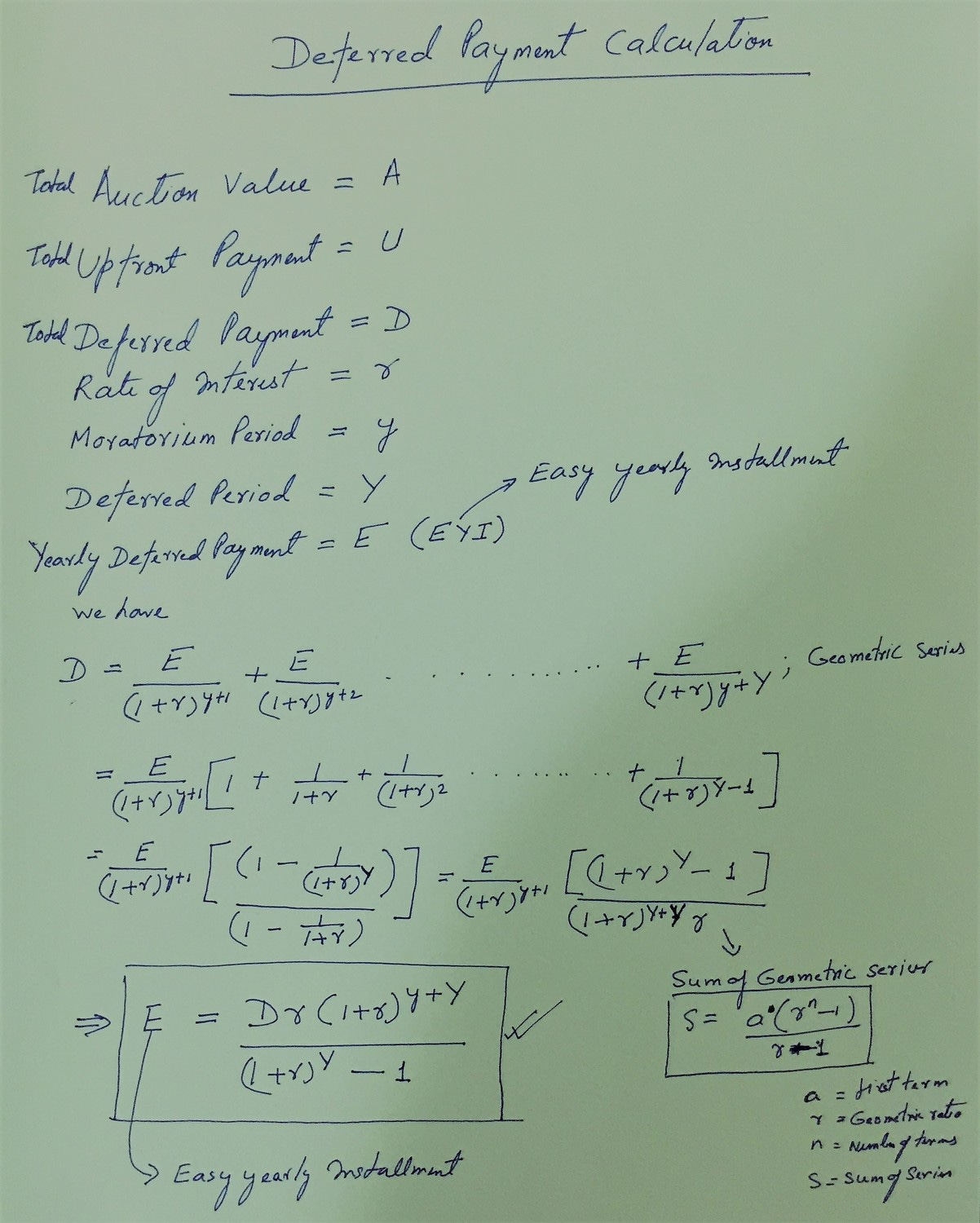

Since the price of spectrum applicable to the satellite industry will most likely be a % of their gross revenue, therefore, to make an apples-to-apples comparison, I have assumed that the total auction outflow in all spectrum auctions since 2010 is deferred with a “Zero” period of moratorium at the applicable rate of interest specified in the NIA (Notice Inviting Application). The payment is then spread over a 20-year period with yearly installments calculated based on the formula which is explained in my earlier note dated 18th Nov 2017 titled - Deferred Payment Calculation Formula. Those interested in the fundamentals, i.e. how the formula is derived, can refer to the workings below.

Note, that while caulating the spectrum auction outflow, the assumptions made are different from the actual payment conditions as mentioned in the NIA. However, since the cash flows are taken into account at their applicable interest rates (notified in the NIA), their DCF values will remain unchanged - enabling us to add the outflows of each year’s auctions directly without applying any further discounting. This will enable us to draw a comparison with the satellite operations that are yet to start in India.

The Calculations

The cumulative values of Industry outflows from various auctions since the year 2010, are described below in the following table.

Industry Rev vs Auction Outflow

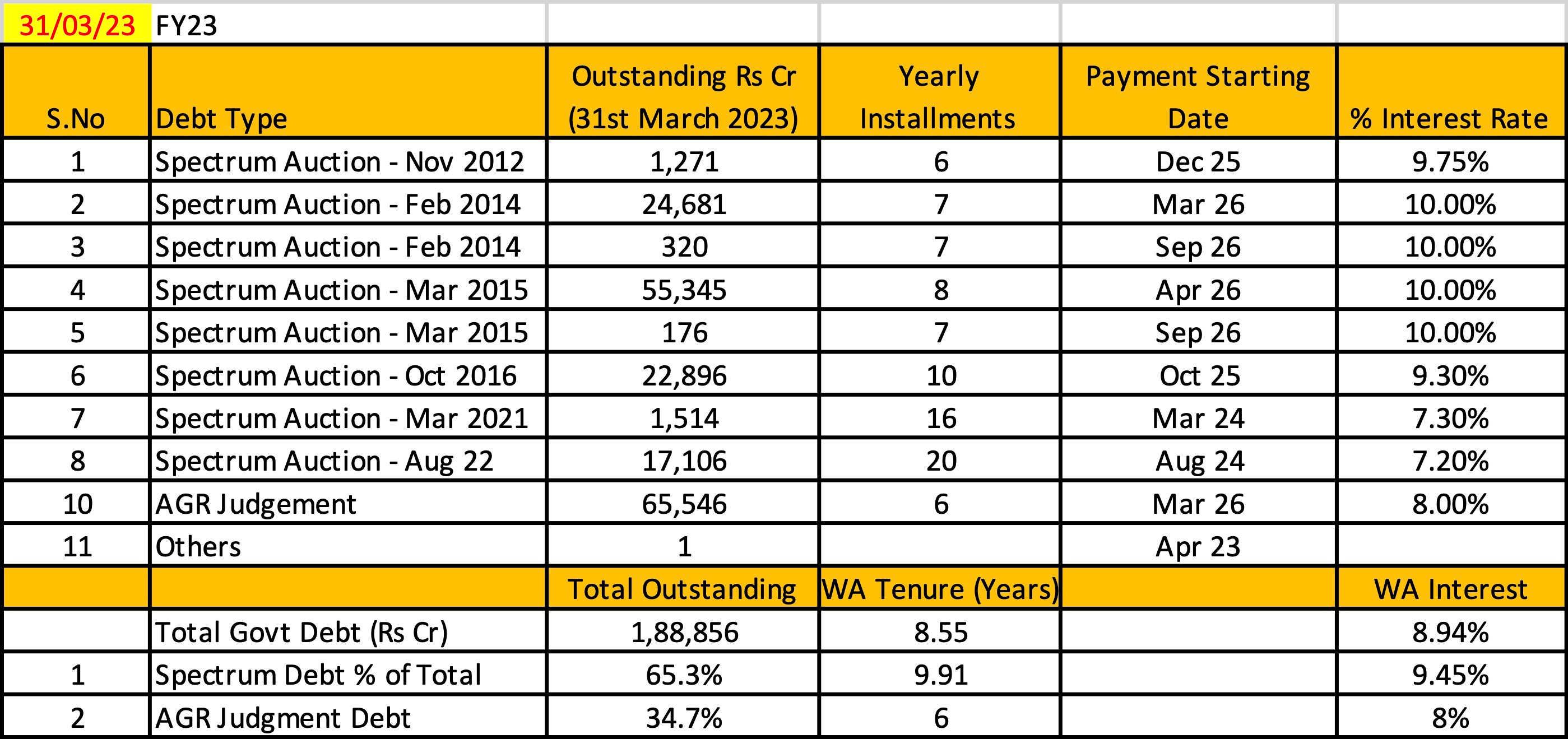

Note, in these workings the actual values of the outflow of all the auctions have been taken, even though we know that a substantial portion of the same has gone NPA. In other words, it is now clear that GOI will NOT be able to recover the full amount that emanated from these auctions. For example, a large portion of VI’s debt (Rs 1.23 Lakh Crs) was accumulated on account of spectrum auctions. See the table below which is extracted from VI’s annual statement, and given the current state of its finances, it seems difficult for VI to repay the same.

VI’s Pending Debt

Similarly, there are many other players like RCOM, Aircel, etc. who went bankrupt.

This means that % outflow to gross revenue of the Industry (which includes only those operators who got spectrum in the auctions) must get pulled down from the final value in the year 2022 of 21.53% to a lower number. Right?

Estimating Satellite Operator’s Projected Revenue

Key Assumption

In order for us to estimate the revenues for the satellite industry we need to project how many subscribers the satellite industry will be able to grab in due course, and at what rate of ARPU (Average Revenue Per User Per Month). Now, for us to be able to calculate this number, we need to visualize whether the satellite service will complement or supplement the existing telecom service. To find the answer to this question, one needs to refer to my earlier article where I explain - Why Satellite Networks Can't Replicate Conventional Mobile Networks. In this note, I have given the reference to the recently launched Huawei Mate 60, and explained why the data speeds experienced by it are so low. But to dive a little deeper into this, we need to answer the following question.

What are the fundamental requirements for satellite services to match terrestrial 5G services? Finding the answer to this question will give us a vital clue - enabling us to make some informed projections of the satellite services market in India.

Requirement 1 - Satellites need to be located in NGSO (Non-Geosynchronous Orbits) to reduce latency (the height of NGSO is in 000’ Kms vs 36K km of GSO), thereby mitigating the cost of retransmission of signals. Why? Only then efficient codecs can be used to drive increased data speeds.

Requirement 2 - Satellites need to operate in high-frequency bands, as only then can drive huge data speeds. Note, ONLY high-frequency bands have a large quantum of spectrum needed to increase throughput.

Therefore, for satellite services to become an alternative to existing 5G services, these need to be integrated into an ordinary commercial mobile phone - which is technically extremely difficult to an extent impossible as has been explained in my earlier article.

Even companies like AST who claim to successfully demonstrated 5G services using NGSO satellites will find it difficut to scale, as they are most likely using low-frequency band (with very little 2x30 MHz of spectrum), and will find it hard deploy a very large number of satellities for it to cover the globle, given huge size of these satellites compared to that of SpaceX. Based on the artcile in the link, their projected number of Total Satellites is just 100, compared to 42K of SpaceX.

Hence, we can safely conclude that satellite services will only complement 5G services and they will never be able to compete with them any time in the future

Satellite Revenue Projection

Using the key assumption above - that satellite will not compete with 5G services, I have made an attempt to estimate the revenues for the satellite industry in the years to come. For this, I have used the latest article published in CNBC dated 13th Sept 2023, which talks about the total subscriber base of SpaceX as 1.5 million subs with an average terminal cost of $600 and ARPU/month of $100. Also, to estimate the year 1 subscription I have picked up Starlink’s projection for India of Nov 2021, wherein it was claimed that it will have 200K subs by Dec 2022, 80% of which will be in the rural areas. The subscribers and revenue projections for SpaceX are estimated in the table below (assume - subs growth rate of 25%, and ARPU drop rate of 10%).

Now, with SpaceX having the highest density of satellites globally, it is fair to estimate that their revenue market share in India will be anything between 50 to 70%. Even if we take a conservative estimate of 50% MS, the total satellite industry’s yearly revenue projection in India will be just over Rs 10,000 Cr in the next 10 years.

Also, we know that the telecom industry is paying 22% revenue share in the year 2022. Assuming that 30% of this is NPA, then the % Outflow on account of spectrum auction becomes 15% of the telecom industry’s total revenue.

If we assume that this 15% remains constant with time, then the satellite industry with just Rs 10 K total revenue should pay a Total % Rev Share for Spectrum = 0.54% (10*15/277). Doubling the Satellite Industry’s Total Revenue to Rs 20 K will upscale the outflow on account of spectrum usage to just 1%.

Conclusion

The preceding discussion unequivocally demonstrates that the Satellite Industry's share of revenue derived from spectrum utilization in India must not exceed 1% in total, whether allocated through auctions or administrative means. This imperative is vital for the industry's overall health, enabling it to provide top-tier services to the Indian consumers.