Navigating Fiscal Waters: Assessing the Challenges in India's Budget Projections for 2024-25

Navigating Fiscal Waters: Assessing the Challenges in India's Budget Projections for 2024-25

The recent budget aims to strengthen India's fiscal stability, but achieving this requires careful management of optimistic projections and potential economic challenges.

A key highlight of the recent budget announcement was the reduction in the central government's fiscal deficit, which was revised from the previously projected 5.12% in the February 2024 budget to 4.9% of the GDP. In absolute terms, the deficit is now anticipated to be Rs 16.13 lakh crore, down from the earlier estimate of Rs 16.85 lakh crore. This represents a significant fiscal contraction of Rs 72,000 crore in the July 2024 budget update. Remarkably, this adjustment has been achieved despite an increase in total expenditure from Rs 47.66 lakh crore to Rs 48.21 lakh crore—an uptick of Rs 55,000 crore. The government managed to offset this by boosting its revenue collections from Rs 30.8 lakh crore to Rs 32.07 lakh crore, an increase of Rs 1.27 lakh crore. When the additional revenue of Rs 1.27 lakh crore is balanced against the Rs 55,000 crore hike in spending, the resulting fiscal improvement stands at Rs 72,000 crore, aligning the deficit to the new target of 4.9% of GDP. The aim of this article is to analyze the robustness of this projection. We will explore the likelihood of maintaining this revised figure, the potential risks of deviation, and the specific budgetary or economic factors that could impact these fiscal outcomes.

Risk No1 - Nominal GDP Projections

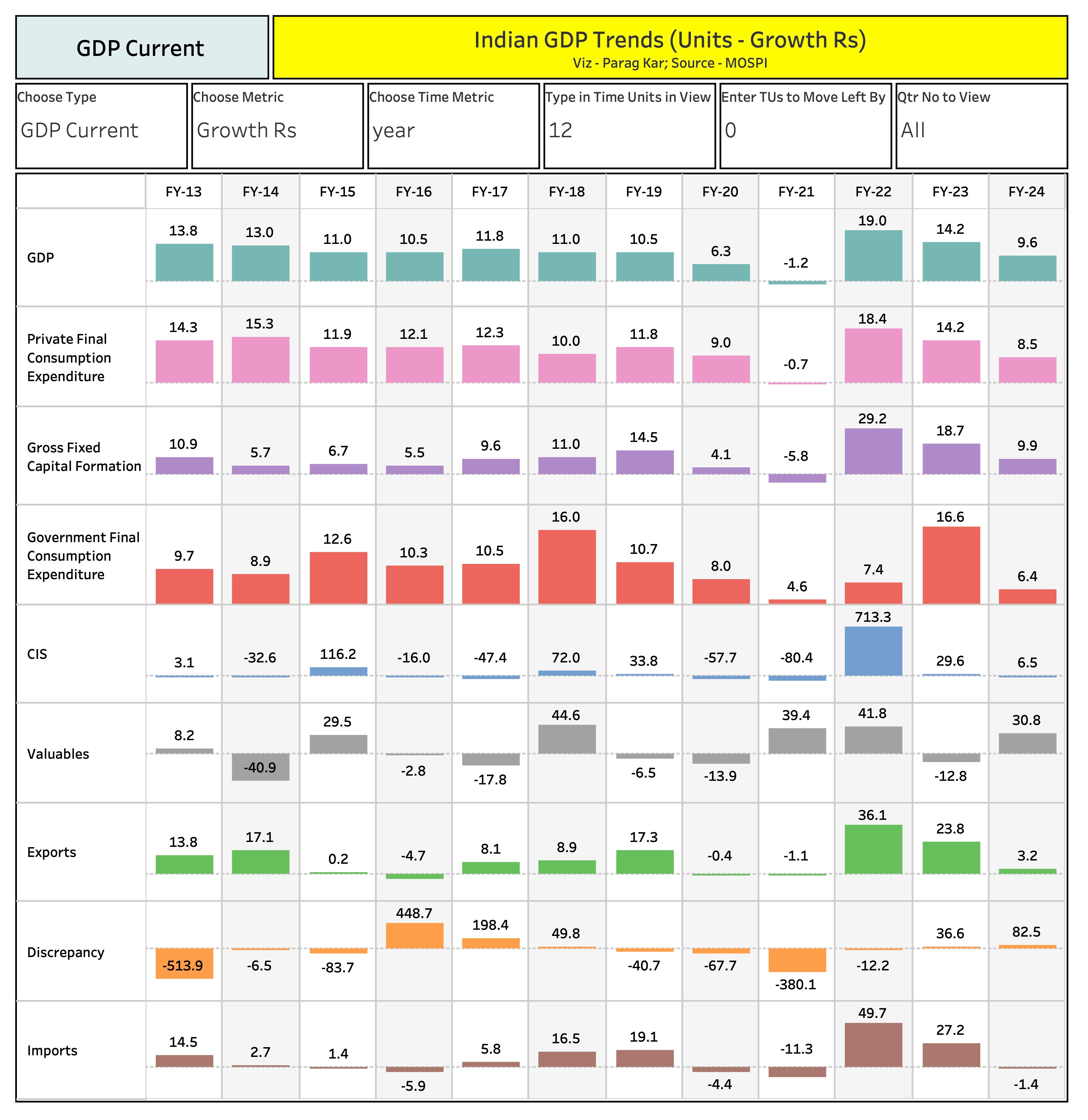

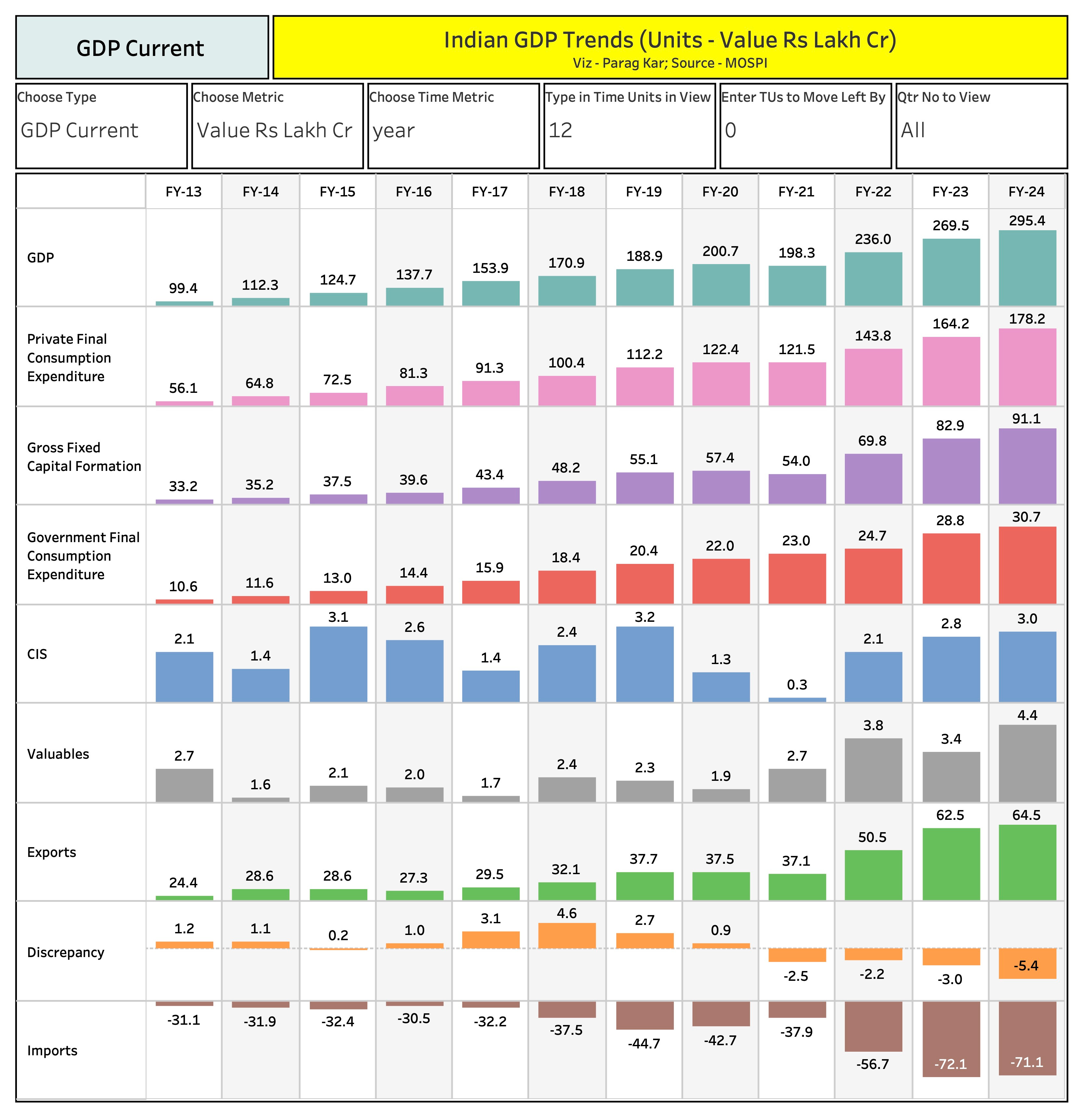

The foundational nominal GDP figure used to derive the 4.9% fiscal deficit projection is Rs 329.18 lakh crore (16.13/0.049), indicating an expected growth of 11.43% (calculated as (329.18 - 295.4) / 295.4). This projection appears optimistic, particularly in light of last year's growth rate of just 9.6%.

Reviewing the trend chart of nominal GDP growth since FY 2013 could suggest that an 11.43% increase is feasible, especially considering the growth rates of 14.2% in FY23 and 19% in FY22. However, these figures are potentially misleading as they were calculated from a reduced base due to the economic impact of COVID-19. A more accurate reflection can be found in the pre-pandemic years, where nominal GDP growth ranged between 6.3% and 13.8%.

Yet, even this broader historical context may not provide a full picture due to the high volatility in the 'Discrepancy' factor (the difference between Production and Consumption methods for calculating GDP), which has significantly influenced recent GDP calculations (as illustrated in the subsequent chart).

Additionally, a critical element to consider is the private final consumption expenditure, which accounts for about 60% of total GDP and is currently at its lowest growth levels - 9.9 % (FY24). This factor alone could undermine the validity of an 11.43% GDP growth assumption and, consequently, any deviation from this growth rate could further inflate the fiscal deficit as a percentage of GDP.

Risk No. 2: Projections of Interest Payments

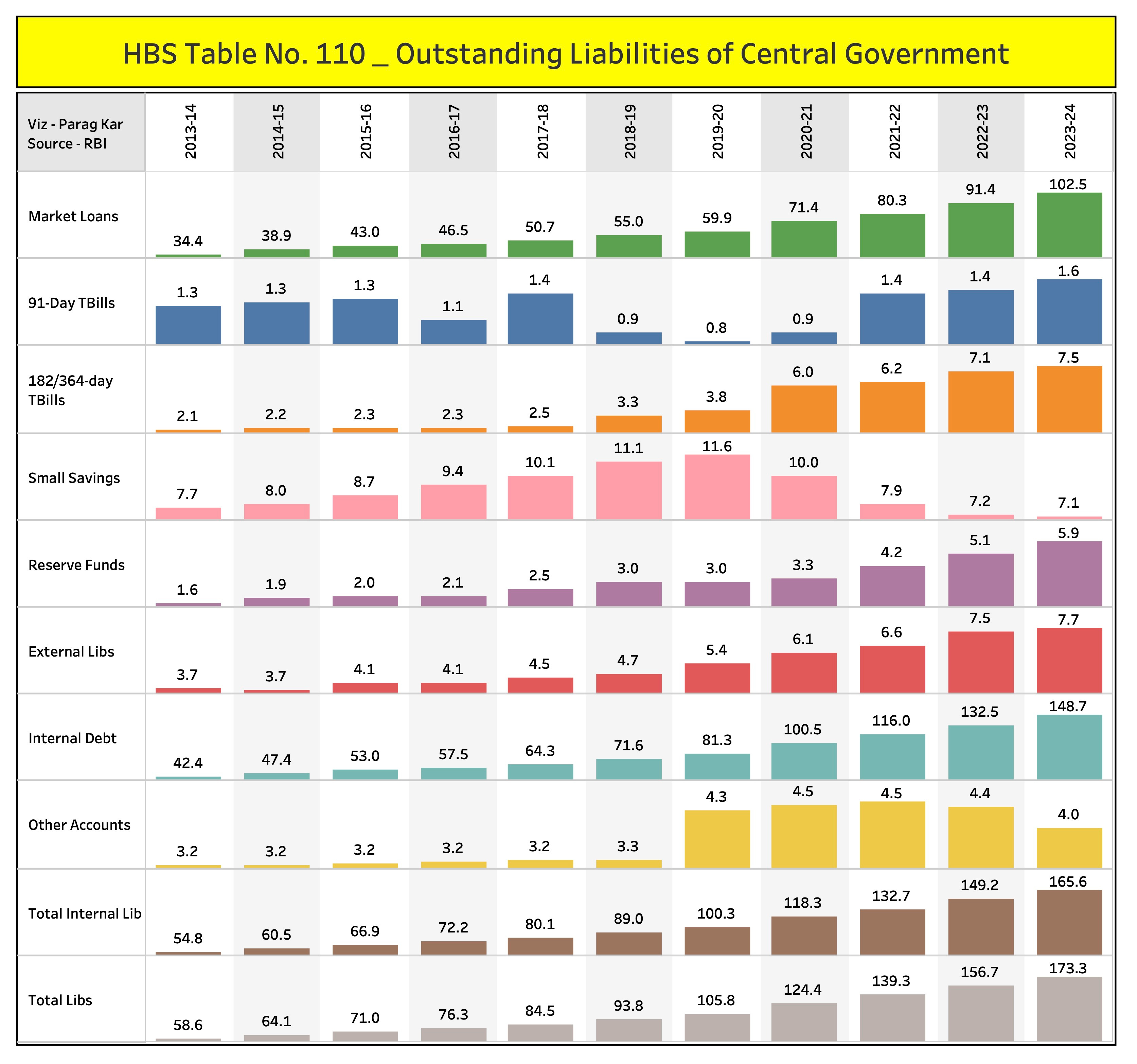

In the revised budget, the Central Government has reduced its interest payment obligations for FY 2024-25 by Rs 27,000 crore to Rs 11.63 lakh crore, down from the February 2024 projection of Rs 11.9 lakh crore. A significant portion of these savings, approximately Rs 12,000 crore, originates from market loans, which constitute nearly 60% of the government's total internal liabilities. These loans were historically taken at fixed interest rates to finance fiscal deficits. (See Chart below on government market borrowings for detailed figures and trends). Additionally, Rs 9,300 crore in savings come from short-term debt instruments like Treasury Bills, though their feasibility is questionable given their dependence on the volatile RBI repo rates and the current high food inflation.

Other minor savings include Rs 1,500 crore related to the Sovereign Gold Bond scheme of 2015 and prepayment premiums for debt reduction, as well as anticipated savings of Rs 5,500 crore from small savings deposit certificates and operational expenses. Analyzing the market loans specifically, the projected Rs 16,000 crore saving in interest payments corresponds to a decrease in bond yield by about 16 basis points, based on the outstanding value of 102.5 lakh crore at the end of FY 2023-24. (Refer to Chart below showing a snapshot of outstanding liabilities in various categories as of the end of FY 2023-24).

Given the historical context of loans taken at interest rates above 7%—except during FY20 to FY22 when inflation and repo rates were lower—it is critical to assess whether such savings are realistically sustainable. Additionally, the significant projected savings of Rs 9.3 K Cr on short-term instruments like T-bills, which are highly dependent on RBI’s repo rates, seem overly optimistic in the current economic climate. Unless extraordinary developments occur, revisiting the original February 2024 budget projections might be necessary.

Risk No. 3: Major Subsidies Projections

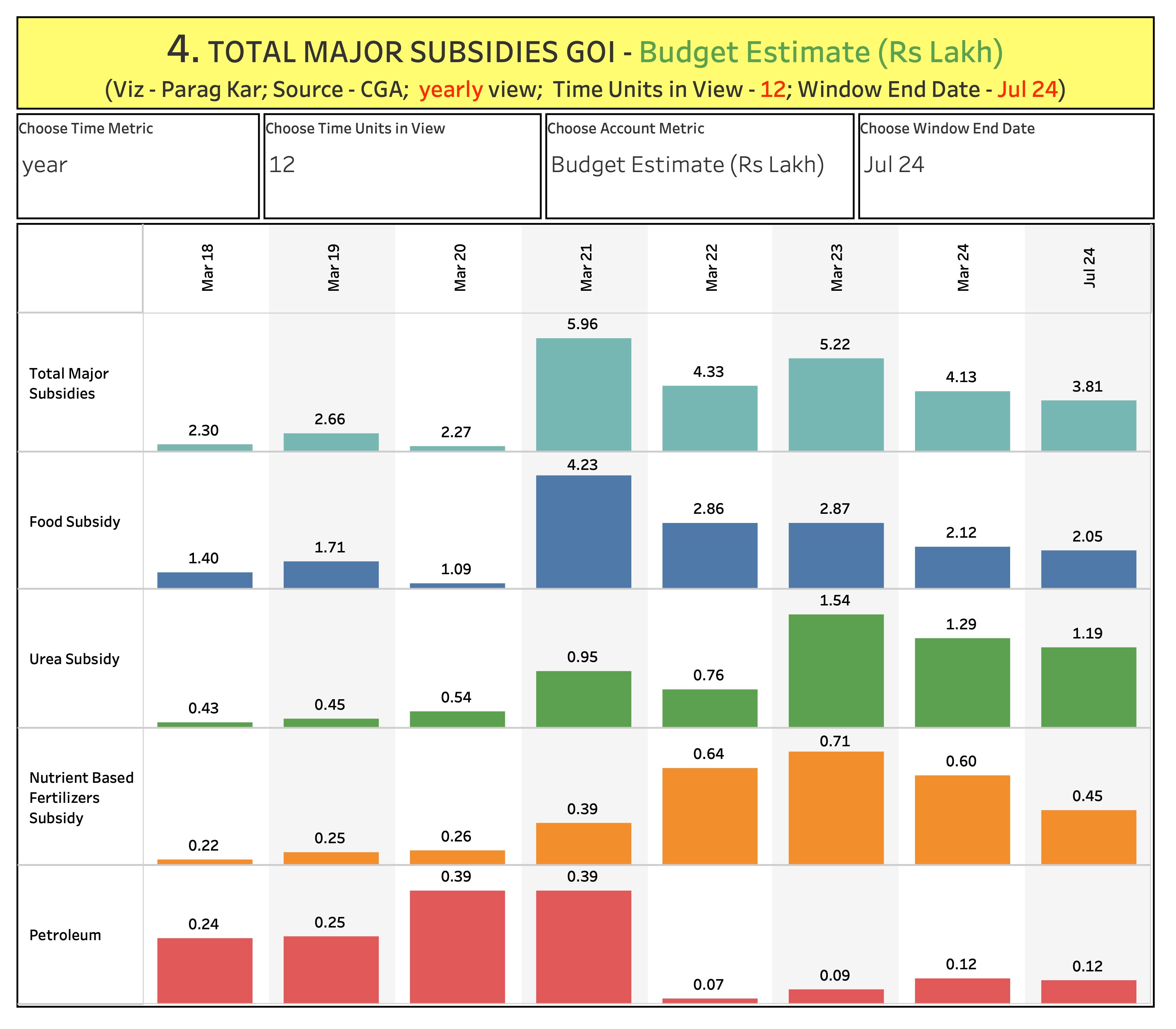

Maintaining fiscal prudence requires accurate projections of key subsidies. Prior to the COVID-19 pandemic, subsidy figures were maintained within a reasonable range of Rs 1.91 to Rs 2.23 lakh crore, representing 1 to 1.4% of GDP. Post-pandemic, these numbers escalated to 3.48% of GDP but were quickly reined in to below 2%, and down to 1.4% by the end of the last fiscal year. (Refer to the accompanying chart for a graphical representation of these trends).

For this fiscal year, the subsidies are projected at Rs 3.81 lakh crore, equivalent to 1.15% of GDP, aligning with pre-COVID levels. Achieving this target would be commendable, given the current challenges of high food inflation and the private sector's restrained investment due to a lack of demand and ongoing job crisis. These structural issues are persistent and are unlikely to resolve quickly, raising the possibility that subsidy projections may need adjustment. The government may face the necessity to revise these figures upwards if it needs to allocate more resources to support the populace amidst uncontrollable food price hikes and to continue aiding farmers, thereby either driving up the fiscal deficit numbers or cutting down on development schemes - both are equally bad.

Conclusion

The recent budget represents a strategic effort to bolster fiscal prudence within the Indian economy—an essential measure to maintain and potentially enhance the country’s creditworthiness and attractiveness to global investors. With FDI flows at a low, projecting a responsible fiscal image is crucial to regaining investor confidence.

However, the execution of this budget is not without significant challenges. The outlined risks, from optimistic GDP growth projections to potential overestimations in subsidy reductions and interest payments, pose substantial threats to maintaining the targeted fiscal deficit. These factors may compel the government to make tough choices: either revise the fiscal deficit targets upwards or implement cuts in vital developmental schemes. Each choice carries significant implications, particularly at a time when the nation is grappling with structural issues such as jobless growth, rural distress, high food inflation, and dwindling disposable incomes.

As we navigate these complex economic times, it becomes a collective responsibility to ensure that the funds allocated are used with maximum efficiency. It is imperative for all stakeholders, from government officials to citizens, to work together to prevent wastage and ensure that every rupee is spent in a way that furthers the welfare of India and its people. Only through vigilant oversight, rigorous implementation, and community engagement can we hope to meet the ambitious goals set forth in this budget and foster a sustainable economic environment.